Are you trying to maximize your healthcare budget while maintaining access to quality care? Health Savings Accounts (HSAs) could be the solution for you. They offer substantial financial advantages and allow more flexible and affordable access to various medical services.

But what is an HSA — and how does it work? Learn about HSAs: eligibility, contribution limits, and smart ways to manage your benefits. Get informed now to make the best decision about setting up your health savings account!

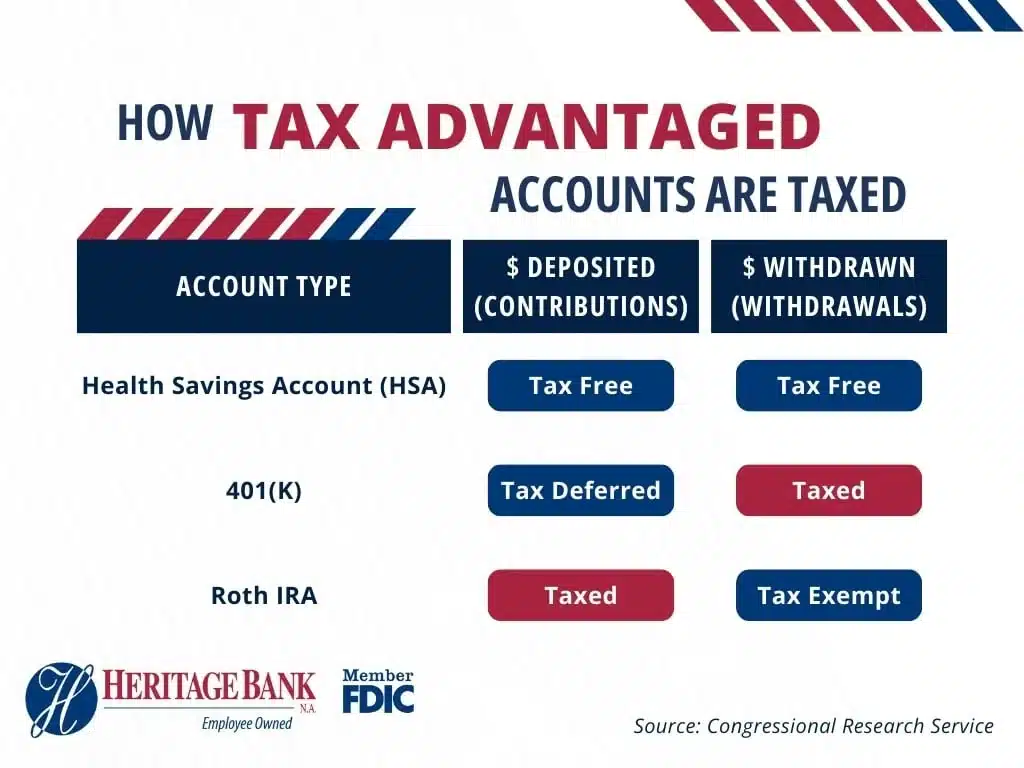

What is a Health Savings Account (HSA)?

A Health Savings Account is a tax-advantaged savings account used to pay for medical expenses. You can make HSA contributions pre-tax, so you don’t pay taxes on your contribution. Furthermore, if you use withdrawals from an HSA for qualified medical expenses, they remain tax-free. You, the employee, own HSA accounts, not your employer.

How does an HSA work?

Your contributions to the account are deductible from your federal income taxes and, in some states, your state income taxes. Choose the HSA account from a reliable bank, like Heritage Bank NA, to suit your needs. Once selected, work with your HR department to arrange tax-free deposits into your HSA.

Learn how to utilize your funds effectively. Heritage Bank NA’s account provides a convenient debit card for seamless use.

What expenses can an HSA cover?

The Internal Revenue Service (IRS) states that individuals can use HSAs to pay for:

-

- Co-pays, deductibles, prescriptions, and other medical costs not covered by insurance.

- Eligible medical expenses

- Health insurance premiums under COBRA continuation coverage

- Health insurance premiums while receiving unemployment compensation.

- Medicare Parts A, B, C & D premiums (for those ages 65 or older only)

- A qualified long-term care insurance contract

Section 213(d) of the Internal Revenue Code defines eligible medical expenses for HSAs.

A complete list is available from the IRS in Publication 502 (Medical and Dental Expenses) by visiting www.irs.gov

Do HSA funds expire?

UNLIKE OTHER MEDICAL SAVINGS ACCOUNTS, your HSA contributions do not expire at year-end or when you change jobs. Your remaining balance will not expire if you switch to a non-eligible health insurance plan or change employers. Your contributions are yours for the rest of your life.

Contribution limits and deadlines for HSAs

The IRS sets the amount you can contribute each year and changes annually. In 2023, the maximum contribution limit for an HSA is $3,850 for an individual and $7,750 for a family. Individuals 55 and over can contribute an additional $1,000 in catch-up contributions. You can only contribute this amount to your HSA each year, but all contributions roll over from year to year.

For 2025, the maximum contribution limit for HSA will be $4,300 for an individual and $8,550 for a family. Individuals 55 and over can contribute an additional $1,000 in catch-up contributions.

You generally have until the tax filing deadline to contribute to an HSA. For the tax year 2024, you can make contributions until April 15, 2025.

Some things to be aware of with an HSA account?

-

- Use your HSA funds wisely to avoid tax penalties. If you are under 65, you will face a 20% penalty and income taxes for using funds on ineligible expenses. If you are 65 or older, you will not be penalized for using HSA funds on unauthorized expenses. However, you still have to pay income taxes.

- Monthly service fees may apply. There are no fees if you sign up for eStatements or electronic statements.

- You can use your HSA in conjunction with a qualifying High Deductible Health Plan.

What is the difference between HSA and FSA?

While an HSA (Health Savings Account) and FSA (Flexible Spending Account) sound similar, they have crucial differences.

HSAs are tax-advantaged accounts that either you or an employer can open and contribute to. HSAs allow you to make pre-tax contributions and take tax-free withdrawals to pay for covered care.

You can invest money in an HSA, which will grow over time. Once you turn 65, you can withdraw the money without penalties, but the regular tax rate will apply to it. You can use an HSA in conjunction with a qualifying High Deductible Health Plan.

You can put money into FSA before taxes and take it out without paying taxes, but only employers can start one. These accounts serve as short-term savings accounts rather than an investment account. At the beginning of the year, you need to choose how much money to put in. If you do not use it for medical care during the year or soon after, you won’t get it back.

Setting up and managing your HSA with Heritage Bank NA

Heritage Bank’s HSA is a personal account that helps eligible individuals save for medical expenses. It earns interest, and you can use it with a High Deductible Health Plan from your insurance provider.

Enroll in a Heritage Bank NA HSA account today.

Enjoy additional features with Digital Banking, a secure and convenient way to manage your Health Savings Account.

Chris Vraa

Chris Vraa has been a mortgage industry professional since 1994 and is known for her drive, dedication, and expertise.

Communication is key for Chris when it comes to her customers. When working with Chris, borrowers will know exactly what’s going on from beginning to the end. Chris knows the ins and outs of the industry from her extensive years of experience, which gives her insight that other loan officers may not have.

“MY PASSION IS HELPING PEOPLE MAKE THEIR SITUATION BETTER, NO MATTER THE CIRCUMSTANCES.” – CHRIS VRAA

Chris loves working with everyone, from the first-time home buyer because it’s all new to them and they’re so excited, to the Physician that might be buying a vacation home. Chris will consistently be there and help her customers navigate the waters. Chris is a trusted leader in the field, and she enjoys working with people to grow and thrive throughout their life.